One of the most fundamental questions I ask people who are about to retire is often a surprise.

What does retirement look like?

That's it. It's not complicated. But this question hits a bit different.

See, it's not about the math. It's about your life. Where you will be. How you will spend your time. What you are genuinely looking forward to.

And it's different for everyone. Even between spouses.

The data backs this up in some uncomfortable ways.

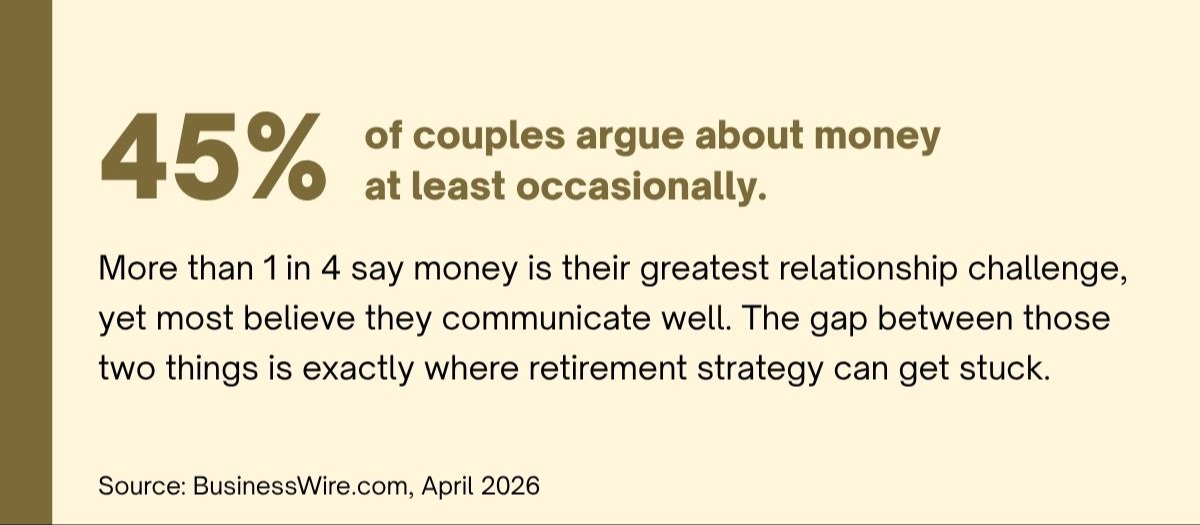

According to Fidelity's 2024 Couples and Money Study, 53 percent of couples who have not yet retired hold conflicting views on how much they need to save. Only 57 percent rate their household's financial health as excellent or very good.¹

These are not small gaps. They are the kinds of misalignments that can quietly derail a retirement strategy.

The Timing Problem Not Talked About Until It’s Too Late

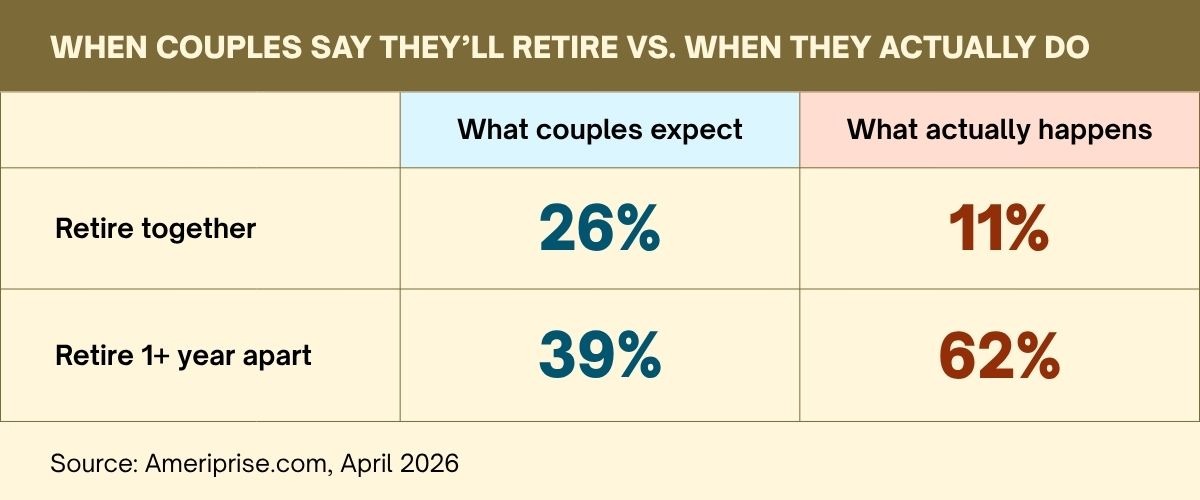

Most working couples expect to retire at the same time or within a year of each other. It is one of the most common assumptions couples make. And one that rarely comes true.²

This gap is real, and there is a lot more to it than a scheduling inconvenience.

When one partner retires and the other doesn't, the household dynamic shifts in ways most couples aren't prepared for. Identity. Structure. Daily rhythm. Who manages the house. Who handles the money. What does the retired partner do with suddenly unstructured days.

Fortunately all of these questions can be answered. But they are far easier to work through before someone has already retired than after.

A staggered retirement done intentionally can actually be a smart financial strategy. The working partner keeps building savings, delays Social Security, and maintains health coverage. Done by surprise, the same situation creates friction that is hard to unwind.

If you haven't had these conversations yet, here are a few good places to start.

These are not questions with obvious answers. And in many cases, couples assume they agree when they have never actually asked.

Where Will We Live?

One partner may have spent years quietly looking forward to a warmer climate. The other may have assumed they were staying in the house where they raised their family. Cost of living, proximity to family, and access to medical care all depend on this one question having a real answer.

What Does a Typical Day Look Like?

Retirement removes the structure most people have used to organize their lives. For some that's a relief. For others it's destabilizing in ways they didn't anticipate. Board service, consulting, a creative practice, a physical commitment, a volunteer role. These are not hobbies. They are sources of identity worth thinking through together before the first day of retirement arrives.

Worth noting. Couples who suddenly spend every hour together after decades of parallel busy lives sometimes need more intentional structure around both togetherness and individual space than they expected.

What Will Our Healthcare Costs Look Like?

According to Fidelity's 2025 Retiree Health Care Cost Estimate, a couple can expect to spend roughly $345,000 on healthcare over the course of retirement.³ Spread across 20 or more years that works out to somewhere around $17,000 annually. Not unreasonable. But it does require a plan.

Medicare is not as simple as most people expect. There are multiple parts, coverage gaps, and premium surcharges for higher income earners that can catch couples off guard. Couples with an age gap may also face a coverage window where one partner is not yet eligible.

And this is before potential long term care needs.

Do We Have a Plan for Potential Extended Care Needs?

According to the U.S. Department of Health and Human Services, 56 percent of adults turning 65 are expected to need some form of long-term care during their lifetime.⁵ And according to Morningstar research, a couple facing extended care expenses sees their wealth decrease by an average of 21 percent over nine years.⁶

These conversations are much easier to have outside of crisis mode. The earlier you plan, the more options you have and the more control you keep.

The question to answer together is not which facility would we prefer. It is what is our financial strategy if this happens, and have we done anything to prepare.

How Does Social Security Fit Into Our Income Strategy?

Social Security is insurance against outliving your income. It was never designed to be a retirement income plan on its own. And for most couples we work with, it plays a supporting role in a much larger income strategy.

What matters most is understanding what each partner is entitled to and how those benefits interact. The timing of one partner's claim affects the survivor benefit available to the other. That decision deserves a real conversation, not a guess.

The chart below shows the range of what is possible. But the right answer for your household depends on your income needs, your health, and what the rest of your retirement strategy looks like.

These are all important conversations. But there is one more that ties them all together.

Do We Have a Financial Strategy?

These numbers are alarming. Not because couples don't care. But because the conversation rarely has a natural home. No agenda. No occasion. No one asking the questions that go beyond the numbers.

But your financial future deserves better. And the conversations behind the numbers are the ones that matter the most.

An estate strategy. A financial strategy. A retirement income strategy. Three conversations that are deeply connected and yet for many couples all three remain unaddressed as retirement approaches.

The good news is that by building one cohesive strategy, you typically resolve all three.

Most Couples Are Closer Than They Think

The conversation that happens with a financial professional tends to look different from the version couples attempt on their own. Part of it is having an agenda. Permission to raise things that might otherwise feel too big or too uncomfortable to introduce.

What we consistently find is that most couples are not as far apart as they fear. The partner who wanted the beach house has usually also been thinking about the grandchildren. The partner who wanted to stay put has been wondering about weathering the winters as they get older. The differences are real. But they are negotiable in ways that rarely feel so when they sit unspoken.

The couples who get the most out of these conversations are the ones who come in willing to be surprised by what their partner actually thinks.

Summer is actually a genuinely good time for this conversation. The pace is different. There is room to think. And the conversations that feel large in the abstract tend to become much more manageable once they start.

If you or someone you know have been putting this off, give us a call. It is an honor to be your financial friend. And clarity is just a simple conversation away.

1 BusinessWire.com, April 2026

2 Ameriprise.com, April 2026

3 NewsRoom.Fidelity.com, July 30, 2025

4 NerdWallet.com, January 15, 2026

5 AARP.org, March 12, 2026

6 CFSWV.com, January 2, 2024

7 Financial-Planning.com, April 19, 2024